What does 'owning stock' mean onchain?

They're all called tokenized stocks and they're not the same thing

They're all called tokenized stocks and they're not the same thing.

In a previous piece I looked at where each tokenized asset class stands. Equities stood out as the category with the most raw potential and the least clarity. In 2026, the activity around tokenized stocks has been hard to ignore.

"Buy Nvidia stock at 3am on a Saturday" can make sense to anyone without needing a glossary or a DeFi tutorial, and that's what makes this category different. It's the first one where regular people can see what changes for them.

Kraken, Nasdaq, ICE, and Robinhood all made moves between February and March. The tokenized equities market crossed $1 billion in total value. Even the Wall Street Journal called them "digital tokens that mimic shares." That word, mimic, tells you everything about where the definition stands right now.

Three models, same name

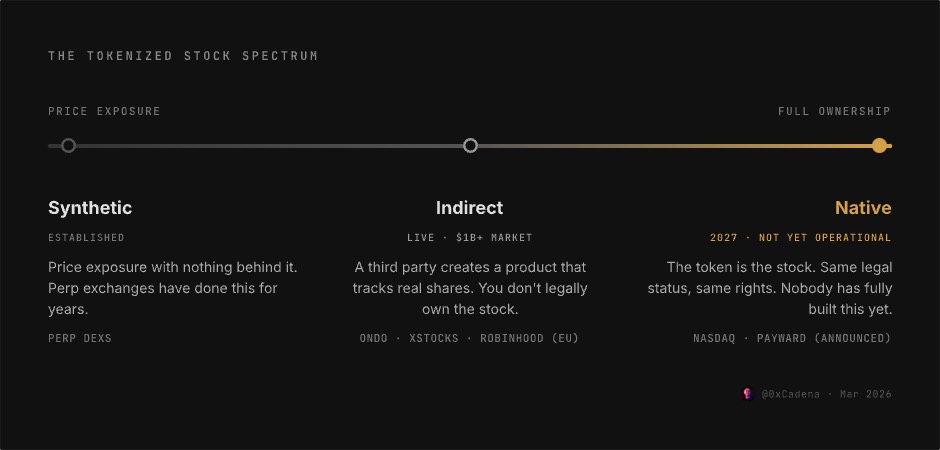

Three approaches exist right now, and they all get called "tokenized stocks."

The first is synthetic, which is just price exposure with nothing behind it.

The second is wrapped or indirect, where a third party creates a product that tracks real shares. You get the price movement, maybe dividends passed through, but you don't legally own the stock. The specifics vary. Ondo Global Markets structures theirs as equity-linked notes, while Kraken's xStocks uses a Jersey-based SPV with shares held 1:1 in custody. Both get called "tokenized stocks," but even within this category they are not the same thing.

And then there's native or direct tokenization, where the token would be the stock itself: same legal status, same settlement, same shareholder rights. Nobody has fully built this for public equities yet. Nasdaq announced a framework for it this month, with Kraken's parent company Payward building the bridge between traditional settlement and onchain rails, but it is not expected to be operational until 2027.

ICE partnered with and invested in OKX to bring NYSE-listed tokenized stocks to OKX users. Robinhood launched its own L2 and has already tokenized around 2,000 U.S. stocks and ETFs for European customers, with a full U.S. launch planned for later this year. DTCC also started building onchain settlement for the securities it already holds.

In about eight weeks, major players made moves in tokenized stocks, and it all looks different.

People chose access over rights

Most indirect models today, including xStocks, are transparent about the tradeoffs. These are exposure products, not direct ownership. No voting, no legal claims to the underlying shares.

The product does what it says it does, and the scale tells you people are fine with that tradeoff. For a lot of the market, access matters more than rights, and whether they technically "own" the stock is secondary to trading it whenever they want from wherever they are.

That model isn't really new. ETFs are a multi-trillion-dollar global market where investors don't directly own shares in the underlying companies. The difference is that ETFs have decades of regulatory structure behind them and indirect tokenized products don't.

Why I think this is the one

Most of the tokenization story so far has been about institutional money. Treasuries, money markets, private credit.

Equities are different. This is where tokenization can talk to everyone. Not just institutions and not just DeFi natives but everyone.

Nobody really has fun with tokenized treasuries. Equities have Tesla, Apple, Nvidia. People already talk about these companies. They don't need to be convinced stocks matter.

Gen Z has arguably skipped traditional brokerages entirely and started with crypto. For them, tokenized stocks aren't a bridge from traditional finance to crypto, they're a bridge the other direction, stocks inside the system they already use.

The indirect model has proven appetite for this asset, but it is a stepping stone. Native tokenization is where I think this goes, and it needs regulatory infrastructure that doesn't exist yet. The people buying these products right now have no idea what they actually own.